AMD (AMD.O) released its third quarter financial report for 2024 (ending September 2024) after the U.S. stock market closed on the morning of October 30, 2024, Beijing time. The key points are as follows:

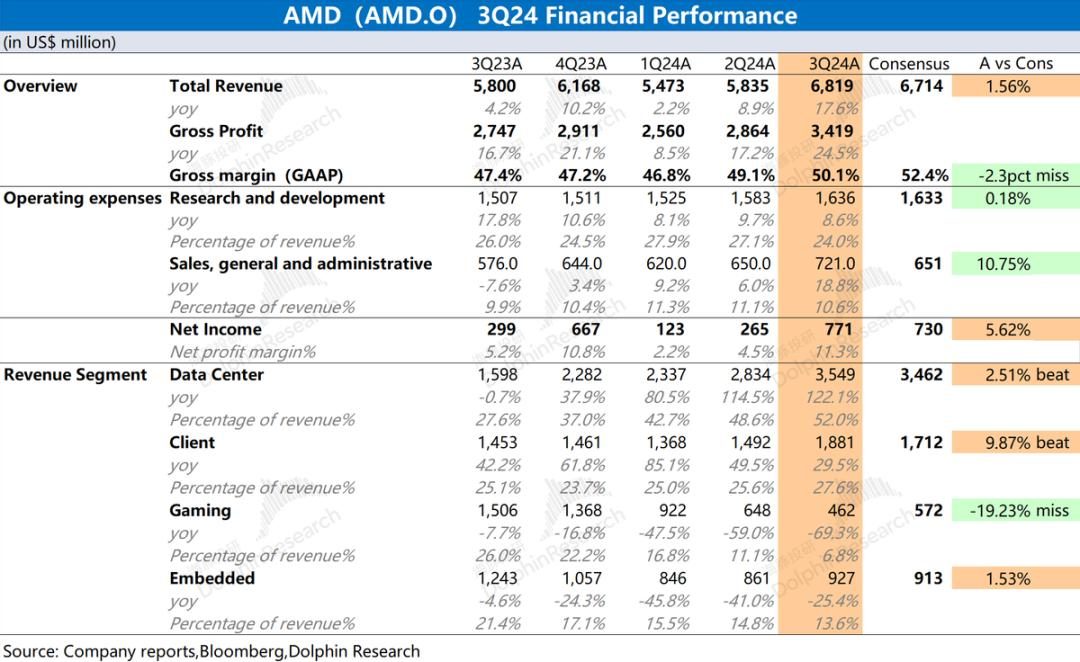

1. Overall performance: revenue and gross profit margin both improved . AMD achieved revenue of US$6.819 billion in the third quarter of 2024, a year-on-year increase of 17.6%, slightly better than market expectations (US$6.714 billion). Quarterly revenue growth was mainly driven by client business and data center business. AMD achieved a net profit of US$771 million in the third quarter of 2024, and the profit side rebounded from the previous quarter, slightly better than market expectations (US$730 million) . Both revenue and gross profit margin have increased, and operating expenses have been relatively stable, driving a rebound in profits.

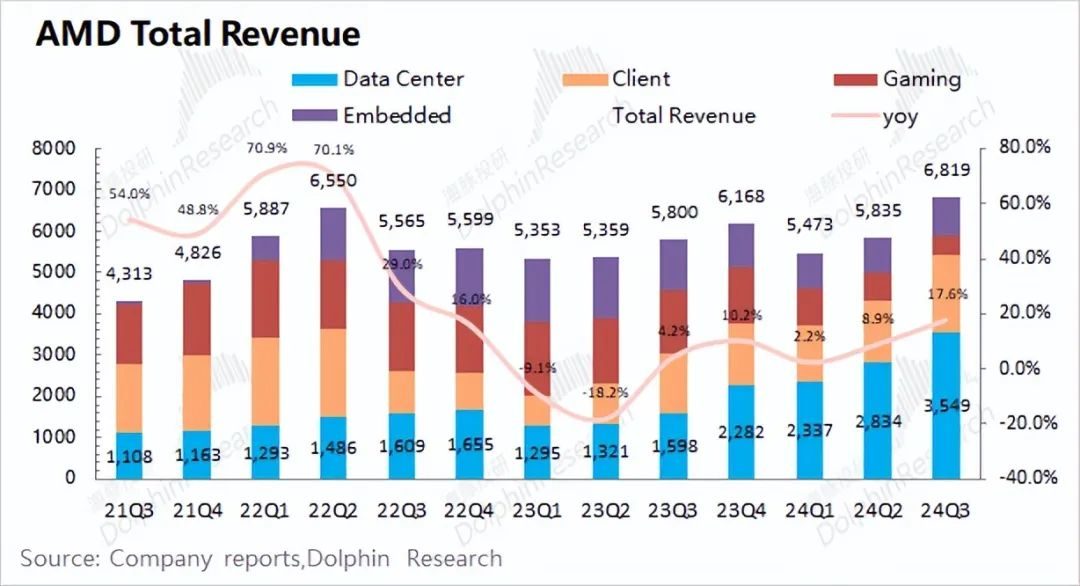

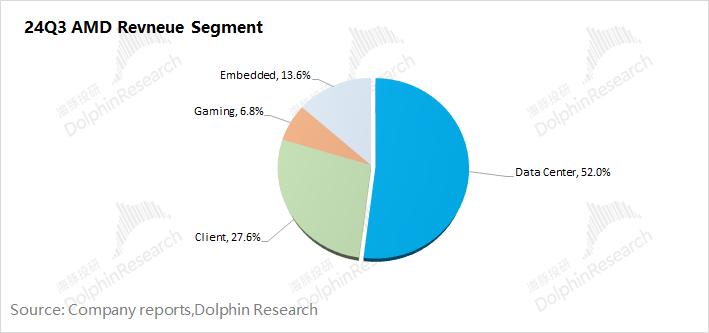

2. Business segmentation: Clients are out of trouble and data centers are at new heights . Driven by the growth of data center and client businesses, the combined revenue of the two businesses accounted for nearly 80%.

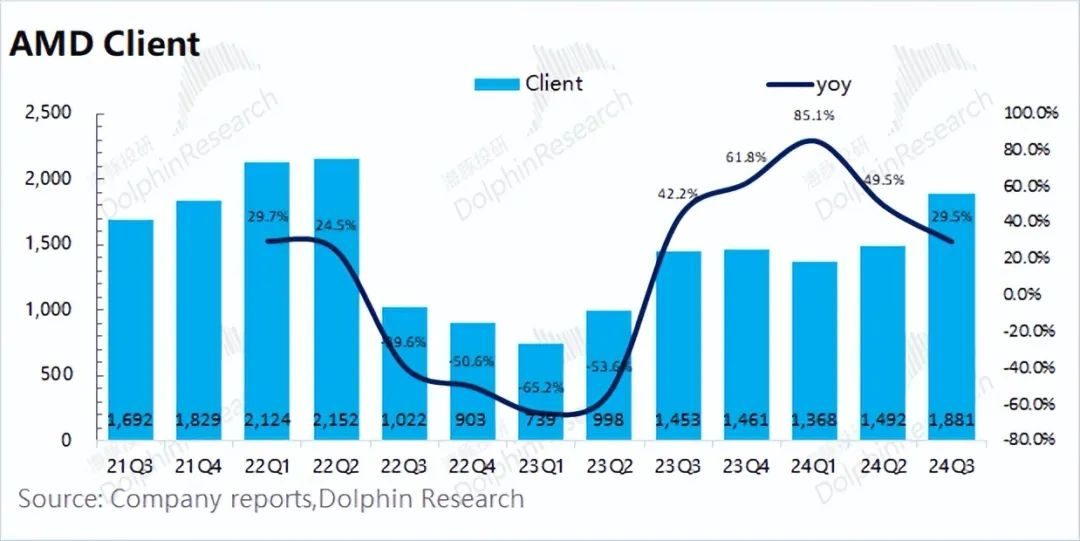

1) The client business got out of trouble: Revenue in this quarter rebounded to US$1.881 billion, a year-on-year increase of 29.5%, successfully getting out of the trough, mainly due to the company's increase in PC market share;

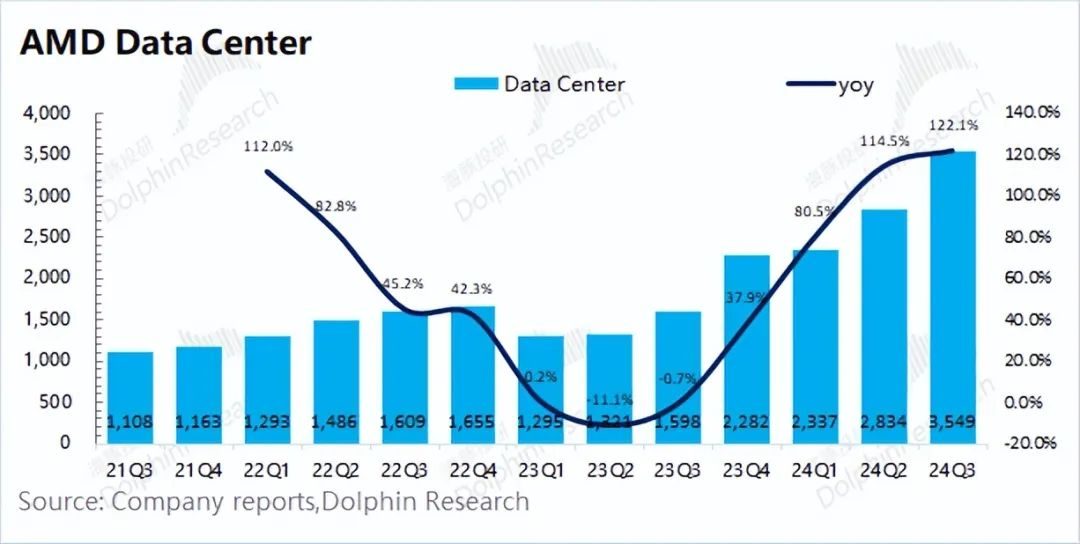

2) New high for data center : Revenue this quarter reached US$3.55 billion, a new quarterly high. This is mainly due to the increase in shipments of the company's related products (GPU and CPU). The root cause is that core cloud vendors still maintain high capital expenditure investments.

3. AMD performance guidance : Expected revenue in the fourth quarter of 2024 is US$7.2-7.8 billion (market expectation is US$7.55 billion) and non-GAAP gross profit margin is about 54% (market expectation is 54.21%). The two core guidance data are basically in line with market expectations. Among them, the revenue side increased month-on-month (5.6%-14.4%), and the growth mainly came from the data center and client business.

Dolphin’s overall view: AMD’s data for this quarter was okay, but it did not give guidance beyond expectations.

AMD's revenue and gross profit margin increased this quarter, mainly driven by the recovery of its two major businesses, data center and client. On the operating expense side, the company's R&D, sales and related expenses have remained relatively stable overall. This quarter, the company's core operating profit returned to more than 1 billion US dollars, and the overall performance has bottomed out.

Regarding the company's core business, specifically: 1) Client business: This quarter achieved US$1.881 billion, an increase of 29.5%. Judging from the single-digit growth of the PC industry, Dolphin believes that the company further squeezed Intel in the PC market this quarter and gained a larger CPU market share (AMD's share in the second quarter of 2024 increased by 3.8pct year-on-year) , driven by new products, it is expected to gain more shares) ; 2) Data center business: reached a new high, reaching US$3.55 billion, mainly due to the strong growth in sales of Instinct series GPU and EPYC series CPU, thus It is speculated that core cloud vendors as a whole will still maintain relatively high capital expenditures this quarter ; 3) Other businesses: The current demand side of game graphics cards has not seen significant improvement, while the embedded business is still in the customer inventory adjustment stage.

Although the revenue and profit data for this quarter were okay, the company failed to provide guidance that exceeded expectations this time . For the next quarter, the company expects revenue in the fourth quarter of 2024 to be US$7.2-7.8 billion (market expectation is US$7.55 billion) and non-GAAP gross profit margin of around 54% (market expectation is 54.21%). The two guidance data are not particularly ideal, and the center of the guidance range is slightly lower than market expectations, which to a certain extent affects the market's confidence in the company and the AI industry chain .

AMD was originally the second supplier in the AI market, and the market itself wanted to see the company catch up with Nvidia and gain more share. While there are signs of relief on the primary supply side of Nvidia, the market is more willing to see AMD's guidance that exceeds expectations to demonstrate the product strength and market demand of MI300. And now such a guideline obviously cannot satisfy the market .

For AMD, Dolphin believes that the main focus of performance is still the data center business, which currently accounts for more than 50% of revenue. The data center business can not only bring business in the short term, but also bring confidence to the market for continued growth in the medium and long term. Since the GPU and CPU end customers in the company's data center business are mainly manufacturers such as Microsoft and Google, Dolphin will still follow up on the capital expenditure plans of core cloud manufacturers. You can pay attention to the company's explanations at the conference call, the specific business progress of data centers and clients, the views on the game graphics card market, and the company's detailed business outlook for the next quarter and the future.

1.1 Income side

AMD achieved revenue of US$6.819 billion in the third quarter of 2024, a year-on-year increase of 17.6%, slightly better than market expectations (US$6.714 billion). The company's quarterly revenue reached a new high, mainly due to the boost of data center business and client business .

The company's share of the PC market continues to increase, driving the company's client business out of the trough. Affected by AI and other related needs, the company's data center business has also seen significant growth in its Instinct series GPUs and EPYC series CPUs.

1.2 Gross profit side

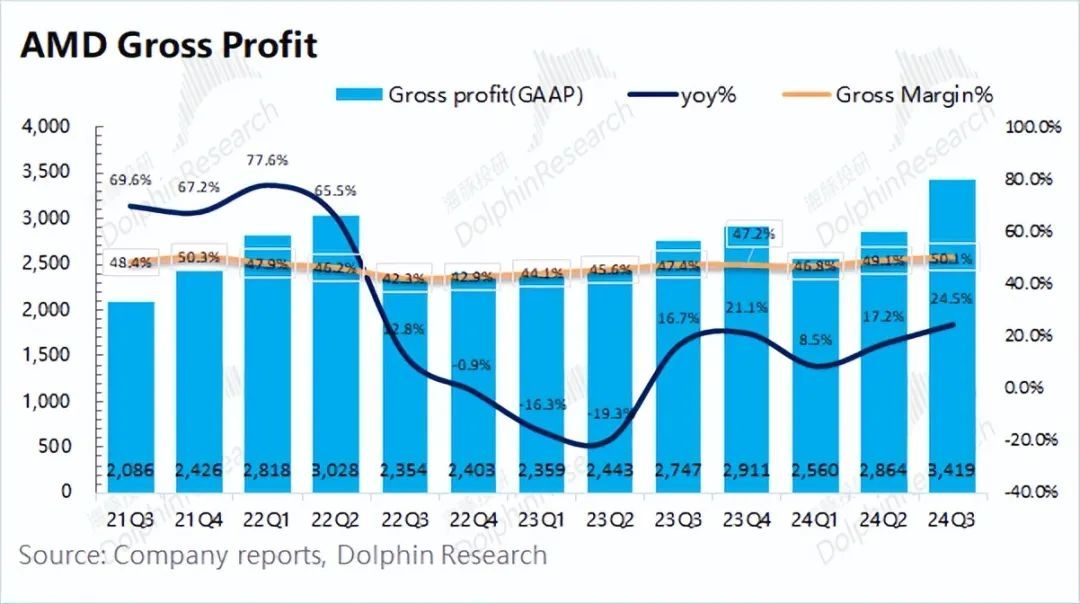

AMD achieved gross profit of US$3.419 billion in the third quarter of 2024, a year-on-year increase of 24.5%. The growth rate of gross profit exceeds that of revenue, mainly because gross profit margin is also increasing.

AMD's gross profit margin in this quarter was 50.1%, a year-on-year increase of 2.7pct, lower than market expectations (52.4%). The gross profit margin rebounded from the previous quarter, mainly due to the increase in the proportion of data center business with higher gross profit margin (currently increased to more than 50%), driving the company's overall gross profit margin growth.

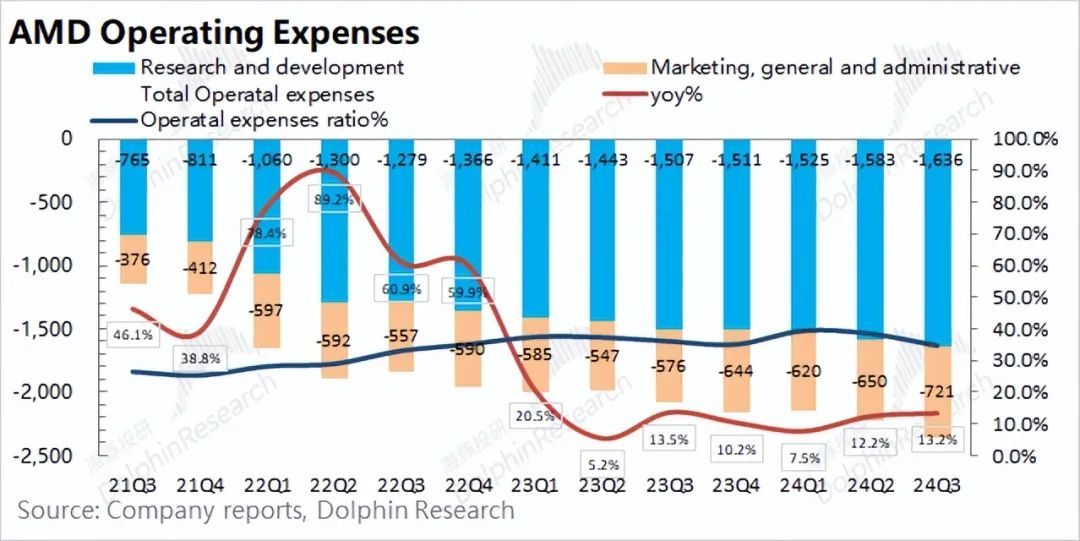

1.3 Operating expenses

AMD's operating expenses in the third quarter of 2024 were US$2.357 billion, a year-on-year increase of 13.2%. Operating expenses also increased month-on-month, but the increase was slightly smaller than the revenue growth.

The specific cost side is broken down into:

1) R&D expenses: The company's R&D expenses in this quarter were US$1.636 billion, a year-on-year increase of 8.6% . R&D expenses have always shown a growth trend. As a technology company, the company continues to attach great importance to research and development. At the same time, due to the growth in revenue, the company's R&D expense rate fell back to 24% this quarter, which is within a relatively reasonable range;

2) Selling and administrative expenses : The company's selling and administrative expenses in this quarter were US$721 million, a year-on-year increase of 25.2% . There is a high correlation between sales expenses and revenue growth, and both increased this quarter.

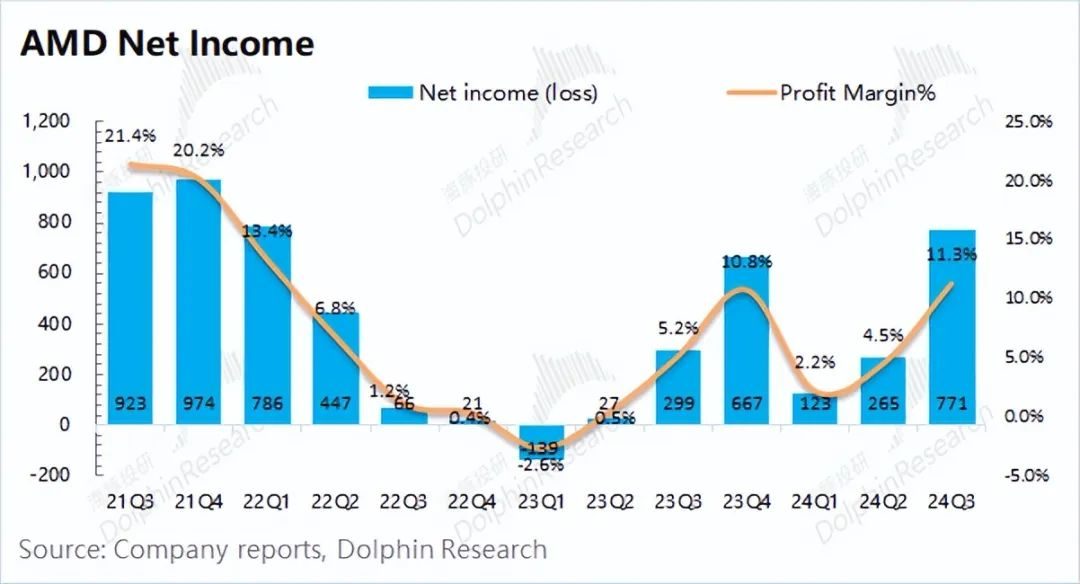

1.4 Net profit

AMD achieved a net profit of US$771 million in the third quarter of 2024. The net profit margin for this quarter was 11.3%, which continued to increase quarter-on-quarter.

As AMD continues to incur large deferred expenses from its acquisition of Xilinx, profits will be eroded for some time to come. As for the actual operating conditions of this quarter, Dolphin believes that "core operating profit" is closer.

Core operating profit = gross profit – total operating expenses

After excluding the impact of acquisition costs, Dolphin estimates that AMD’s core operating profit for this quarter was US$1.062 billion, an increase of 68.3% from the previous quarter. Under the influence of both revenue and gross profit margin growth, the company's overall operating performance has seen a significant improvement. Although the company's gaming graphics card performance was still sluggish this quarter, its client business and data center business both improved significantly.

Among them, when the PC market only grew by single digits, the company's client business revenue increased by 29.5% year-on-year, mainly due to the increase in market share. In addition, while the company continued to ship GPU and CPU products, its data center business hit a new quarterly revenue high.

Looking at the company's business segments, with the growth of the data center business, the proportion has exceeded 50%. The proportion of client business also rebounded to 27.6%, and the proportions of the remaining two businesses fell again.

2.1 Data center business

AMD's data center business achieved revenue of US$3.549 billion in the third quarter of 2024, a year-on-year increase of 122.1%, slightly better than market expectations (US$3.462 billion), mainly due to the company's AMD Instinct series GPU sales and EPYC (Xiaolong) series CPU Strong sales growth.

Combined with the recent event information of Advancing AI 2024, the company will launch: 1) New AMD EPYC 9005 series processors to meet various data center needs and can be used on various platforms of OEM and ODM; 2) AMD Instinct MI325X accelerator , delivering leading performance and memory capabilities for the most demanding AI workloads, with next-generation AMD Instinct accelerators scheduled for launch in 2025 and 2026; 3) Announced $4.9 billion acquisition of ZT Systems to expand data center AI systems business. The latter is committed to providing ultra-large-scale server solutions for cloud computing and artificial intelligence every year, with server shipments reaching hundreds of thousands. Its main customers include Microsoft, Amazon, etc.

In addition, the company further raised its full-year revenue guidance for AI chips from US$4.5 billion to US$5 billion, which also shows that the data center business still has good demand. Since the data center business is mainly affected by the capital expenditures of cloud vendors, Dolphin Jun believes that several core cloud vendors still maintain high capital expenditures in this quarter .

2.2 Client business

AMD's client business achieved revenue of US$1.881 billion in the third quarter of 2024, a year-on-year increase of 29.5%, which was better than market expectations (US$1.712 billion) . The growth of clients is mainly due to the increase in sales of fifth-generation Ryzen CPUs.

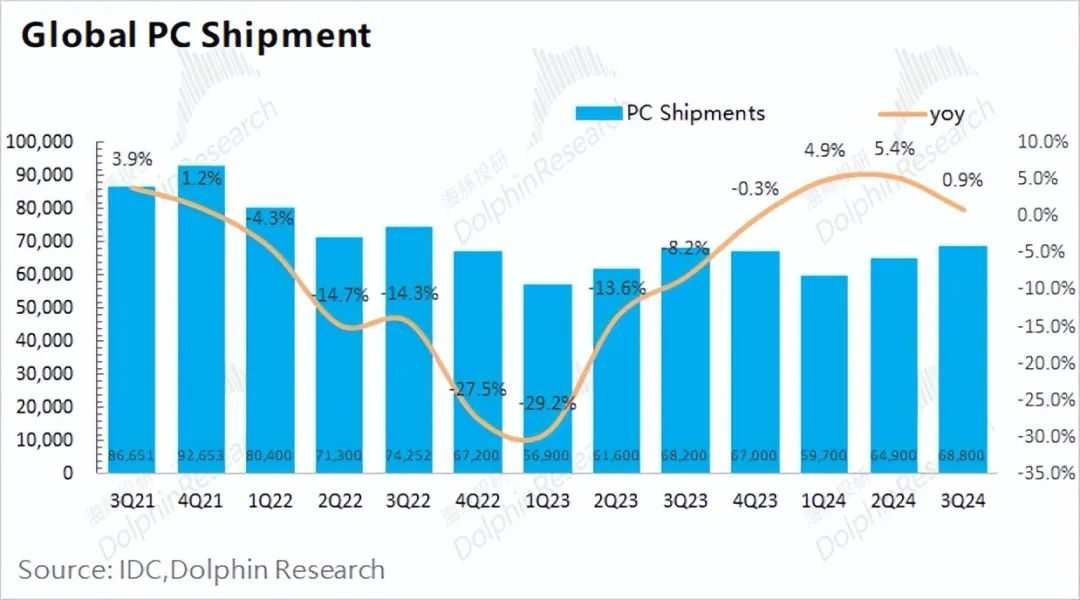

Based on industry data, global PC shipments in the third quarter of 2024 were 68.8 million units, a year-on-year increase of 0.9% . At the same time, AMD's client business has achieved nearly 30% year-on-year growth . Dolphin believes that the main reason is that AMD has gained a larger market share in the PC market this quarter, and is slightly worried about Intel's financial report .

In addition, the company announced the launch of the new Ryzen AI PRO 300 series mobile processors, providing enterprises with next-generation AI PCs with 50+ AI TOPs; and the company is expected to launch the next-generation Ryzen 9000 X3D in the fourth quarter of 2024 processor. With the blessing of computing power and the launch of new products, AMD is expected to gain more market share from Intel and be the first to get out of the trough of the PC business.

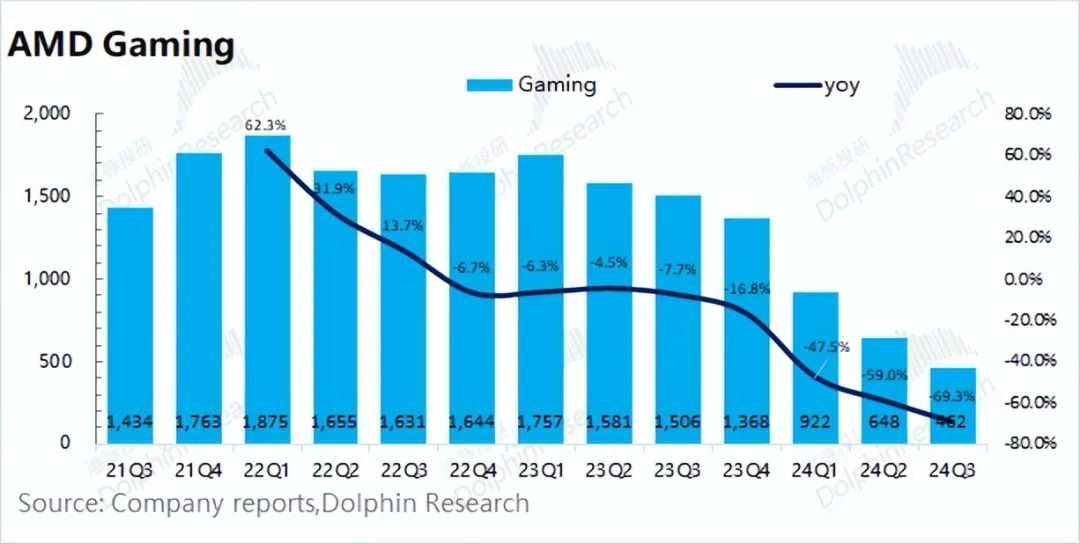

2.3 Game business

AMD's gaming business achieved revenue of US$462 million in the third quarter of 2024, a year-on-year decline of 69.3% and lower than market expectations (US$572 million). The decline in the game business was mainly affected by the decline in semi-custom business revenue.

Although the company's client business has rebounded significantly, the current game business is still weak. Based on the industry situation, Dolphin believes that the PC industry as a whole is in a state of slow recovery, and the demand for game graphics cards has not improved significantly. As for the client business, AMD gained a larger market share mainly due to Intel's "pull-and-pull" performance. As for gaming graphics cards, the company's main competitor is Nvidia, which has no significant share increase.

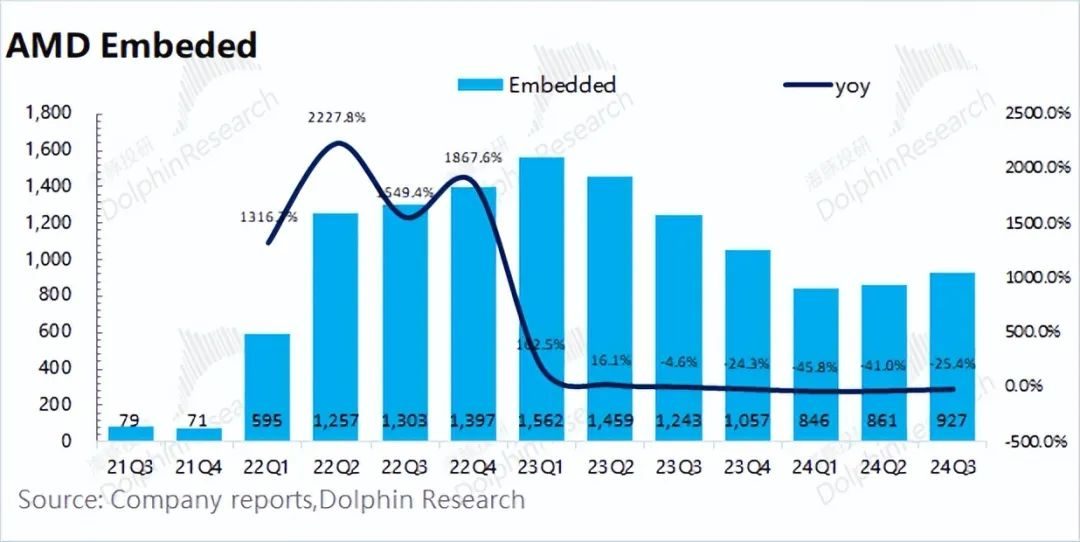

2.4 Embedded business

AMD's embedded business achieved revenue of US$927 million in the third quarter of 2024, a year-on-year decrease of 25.4%, basically in line with market expectations (US$913 million) . The company's embedded business is dominated by the previously acquired Xilinx. Although some downstream demand has improved this quarter, the company is still affected by customers' inventory adjustments, and the company's shipments remain at a relatively low level.