pytorch ts

Version 0.6.0

Pytorchtsは、GluontsをバックエンドAPIとして利用し、時間系列のデータセットを読み込み、変換、バックテストするために、最先端のPytorch時系列モデルを提供するPytorchの確率的時系列予測フレームワークです。

$ pip3 install pytorchts

ここでは、Gluonts Readmeを介してAPIの変更を強調します。

import matplotlib . pyplot as plt

import pandas as pd

import torch

from gluonts . dataset . common import ListDataset

from gluonts . dataset . util import to_pandas

from pts . model . deepar import DeepAREstimator

from pts import Trainerこの簡単な例は、いくつかのデータでモデルをトレーニングする方法を示しており、それを使用して予測を行います。最初のステップとして、いくつかのデータを収集する必要があります。この例では、AMZNティッカーシンボルに言及したツイートのボリュームを使用します。

url = "https://raw.githubusercontent.com/numenta/NAB/master/data/realTweets/Twitter_volume_AMZN.csv"

df = pd . read_csv ( url , header = 0 , index_col = 0 , parse_dates = True )最初の100のデータポイントは次のようになります。

df [: 100 ]. plot ( linewidth = 2 )

plt . grid ( which = 'both' )

plt . show ()

これで、モデルがトレーニングできるトレーニングデータセットを準備できます。データセットは、本質的に辞書の反復可能なコレクションです。各辞書は、おそらく関連する機能を備えた時系列を表します。この例では、最初のデータポイントのタイムスタンプである"start"フィールドで指定されたエントリと、時系列データを含む"target"フィールドのみが1つしかありません。トレーニングには、2015年4月5日の真夜中までデータを使用します。

training_data = ListDataset (

[{ "start" : df . index [ 0 ], "target" : df . value [: "2015-04-05 00:00:00" ]}],

freq = "5min"

)予測モデルは予測オブジェクトです。予測因子を取得する1つの方法は、特派員の推定器をトレーニングすることです。推定器をインスタンス化するには、処理する時系列の頻度と、予測する時間ステップの数を指定する必要があります。この例では、5分間のデータを使用しているため、 req="5min"使用しています。次の時間をprediction_length=12するためにモデルをトレーニングします。モデルへの入力は、各時点でサイズinput_size=43のベクトルになります。また、 epoch=10のdeviceで特定のトレーニングで最小限のトレーニングオプションを指定します。

device = torch . device ( "cuda" if torch . cuda . is_available () else "cpu" )

estimator = DeepAREstimator ( freq = "5min" ,

prediction_length = 12 ,

input_size = 19 ,

trainer = Trainer ( epochs = 10 ,

device = device ))

predictor = estimator . train ( training_data = training_data , num_workers = 4 ) 45it [00:01, 37.60it/s, avg_epoch_loss=4.64, epoch=0]

48it [00:01, 39.56it/s, avg_epoch_loss=4.2, epoch=1]

45it [00:01, 38.11it/s, avg_epoch_loss=4.1, epoch=2]

43it [00:01, 36.29it/s, avg_epoch_loss=4.05, epoch=3]

44it [00:01, 35.98it/s, avg_epoch_loss=4.03, epoch=4]

48it [00:01, 39.48it/s, avg_epoch_loss=4.01, epoch=5]

48it [00:01, 38.65it/s, avg_epoch_loss=4, epoch=6]

46it [00:01, 37.12it/s, avg_epoch_loss=3.99, epoch=7]

48it [00:01, 38.86it/s, avg_epoch_loss=3.98, epoch=8]

48it [00:01, 39.49it/s, avg_epoch_loss=3.97, epoch=9]

トレーニング中、進捗に関する有用な情報が表示されます。利用可能なオプションの完全な概要を取得するには、 DeepAREstimator (または他の推定器)およびTrainerのソースコードを参照してください。

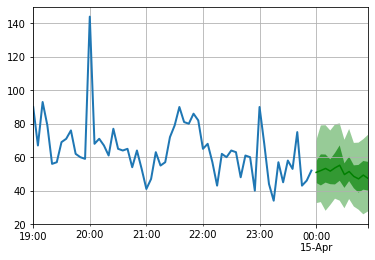

予測を行う準備ができました。2015年4月15日の真夜中に続く時間を予測します。

test_data = ListDataset (

[{ "start" : df . index [ 0 ], "target" : df . value [: "2015-04-15 00:00:00" ]}],

freq = "5min"

) for test_entry , forecast in zip ( test_data , predictor . predict ( test_data )):

to_pandas ( test_entry )[ - 60 :]. plot ( linewidth = 2 )

forecast . plot ( color = 'g' , prediction_intervals = [ 50.0 , 90.0 ])

plt . grid ( which = 'both' )

予測は確率分布の観点から表示されることに注意してください。網掛け部分は、それぞれ中央値(濃い緑色の線)を中心とする50%と90%の予測間隔を表しています。

pip install -e .

pytest test

このリポジトリを引用するには:

@software{pytorchgithub,

author = {Kashif Rasul},

title = {{P}yTorch{TS}},

url = {https://github.com/zalandoresearch/pytorch-ts},

version = {0.6.x},

year = {2021},

}このフレームワークを使用して、次のモデルを実装しました。

@INPROCEEDINGS{rasul2020tempflow,

author = {Kashif Rasul and Abdul-Saboor Sheikh and Ingmar Schuster and Urs Bergmann and Roland Vollgraf},

title = {{M}ultivariate {P}robabilistic {T}ime {S}eries {F}orecasting via {C}onditioned {N}ormalizing {F}lows},

year = {2021},

url = {https://openreview.net/forum?id=WiGQBFuVRv},

booktitle = {International Conference on Learning Representations 2021},

}@InProceedings{pmlr-v139-rasul21a,

title = {{A}utoregressive {D}enoising {D}iffusion {M}odels for {M}ultivariate {P}robabilistic {T}ime {S}eries {F}orecasting},

author = {Rasul, Kashif and Seward, Calvin and Schuster, Ingmar and Vollgraf, Roland},

booktitle = {Proceedings of the 38th International Conference on Machine Learning},

pages = {8857--8868},

year = {2021},

editor = {Meila, Marina and Zhang, Tong},

volume = {139},

series = {Proceedings of Machine Learning Research},

month = {18--24 Jul},

publisher = {PMLR},

pdf = {http://proceedings.mlr.press/v139/rasul21a/rasul21a.pdf},

url = {http://proceedings.mlr.press/v139/rasul21a.html},

}@misc{gouttes2021probabilistic,

title={{P}robabilistic {T}ime {S}eries {F}orecasting with {I}mplicit {Q}uantile {N}etworks},

author={Adèle Gouttes and Kashif Rasul and Mateusz Koren and Johannes Stephan and Tofigh Naghibi},

year={2021},

eprint={2107.03743},

archivePrefix={arXiv},

primaryClass={cs.LG}

}